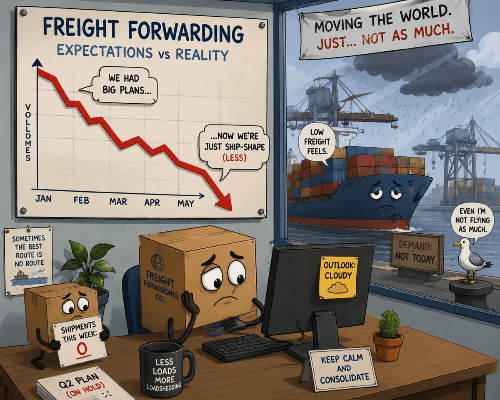

DARIUS AND COMPANY

Freight Volume Decline & Economic Contradictions

by Chat GPT

Question:

If China is down 30% it has to be replaced by something logically, especially if other areas are down 15%. Doesn’t

make sense unless demand is down globally which would be recession unless there are other factors you can tell me but everything you read about we are supposedly booming but at the same time I see BK up etc

Answer:

You are seeing the contradiction correctly. A lot of the headline “economy is booming” narrative and the

freight/logistics reality do not fully line up right now.

Here’s the key:

International freight volumes can absolutely fall hard even while:

• stock markets rise,

• GDP stays positive,

• unemployment stays relatively low,

• and governments say the economy is strong.

Because freight is tied much more to:

• physical goods consumption,

• inventory cycles,

• industrial production,

• housing,

• manufacturing,

• imports/exports,

than to financial asset inflation.

A few things are happening simultaneously:

1. China down does NOT automatically mean replacement volume equals 100%

This is the big misconception.

If China-origin freight falls 30%, replacement sourcing from:

• Vietnam

• India

• Mexico

• Thailand

• Malaysia

• nearshoring

does NOT necessarily fully replace the lost volume because:

• companies order less overall,

• consumers buy fewer physical goods,

• inventories were massively overbuilt after COVID,

• companies are destocking,

• freight rates collapsed so fewer “panic shipments” happen,

• and companies are becoming more efficient with inventory.

So:

• maybe China falls 30%

• replacement countries rise 10–15%

• but total global container demand still drops.

That can happen in a soft industrial recession.

2. Services economy vs goods economy;

The U.S. economy today is heavily service-driven.

People are spending on:

• travel,

• restaurants,

• concerts,

• streaming,

• AI/software,

• healthcare,

• experiences,

instead of:

• furniture,

• TVs,

• appliances,

• imported home goods.

Freight forwarding lives mostly in the GOODS economy.

So Wall Street and GDP can look “fine” while freight feels ugly.

3. Asset inflation can hide weakness

When:

• stocks rise,

• home prices stay elevated,

• AI companies explode upward,

people assume the economy is strong.

But underneath:

• small business bankruptcies rise,

• trucking failures rise,

• freight brokers disappear,

• retail weakness increases,

• office vacancies rise,

• middle-income consumers weaken.

You are probably sensing the “real economy” side because freight forwarding is an early-cycle industry.

Historically, logistics often weakens BEFORE official recession statistics show it.

4. Tariffs create distortion, not always replacement growth

Tariffs can actually REDUCE total trade volume.

Why?

Because:

• some products simply become too expensive,

• importers cancel orders,

• consumers delay purchases,

• businesses reduce inventory,

• sourcing transitions take years.

So instead of:

China -30%, India +30%

you might get:

• China -30%

• India +8%

• Vietnam +6%

• Mexico +4%

• and total global trade still negative.

5. “Booming economy” depends on WHICH economy

Right now there are basically multiple economies:

AI / Tech / Mega-cap stocks — Strong

Luxury travel — Strong

Government spending — Strong

Services — Decent

Industrial/manufacturing — Weak

Freight/logistics — Weak

Trucking — Weak

Housing-related goods — Weak

Middle consumer — Softening

That’s why the signals feel schizophrenic.

6. Bankruptcy increases are a real warning sign

Bankruptcies rising while headlines stay optimistic often means:

• higher interest rates are finally biting,

• weaker companies are running out of liquidity,

• COVID-era cheap money is gone,

• and refinancing debt became difficult.

Freight/logistics especially got addicted to:

• ultra-cheap money,

• huge COVID demand,

• insane container pricing,

• inventory hoarding.

Now the unwind is painful.

My guess personally on U.S.-based international freight forwarding volumes overall:

• probably down somewhere in the 10–20% range from peak normalized conditions depending on sector,

• with China lanes potentially down much more,

• especially for small/mid-sized forwarders without heavy contract logistics or diversified services.

The big globals like Kuehne + Nagel, DHL, DSV, and Expeditors International survive better because they have:

• customs,

• warehousing,

• contract logistics,

• pharma,

• aerospace,

• defense,

• diversified geographies,

• and huge balance sheets.

So....Smaller forwarders feel the pain much faster..

SIGN UP FOR OUR NEWSLETTER